Nearly one in five persons in the United States suffer from a mental illness each year, yet many find it difficult to understand the intricacies of insurance coverage for their treatment. To get the help you require, it is essential to know what your insurance covers for mental health care.

Because different providers have varied reimbursement rules for mental health services, the process of getting paid can be intimidating. To make sure you’re optimizing your benefits, it’s critical to understand the ins and outs of your insurance plan.

People can better manage their mental health care by understanding the complexities of insurance programs and their constraints. The goal of this essay is to give you a thorough understanding so you can make wise decisions regarding your mental health.

Understanding Mental Health Insurance Coverage

You can get the care you require without going over budget if you know what your mental health insurance covers. Benefits for mental health are an essential component of many insurance policies.

Types of Mental Health Benefits in Insurance Plans

Numerous mental health services, such as counseling, therapy sessions, and psychiatric care, are frequently covered by insurance policies. Other advantages like support groups and drug rehab may also be included in some plans.

Between various insurance companies and plans, the details of what is covered can fluctuate greatly. Examining the paperwork for your plan is crucial to comprehending its contents.

Mental Health Parity Laws and Patient Protections

Insurance plans must cover mental health care on a same basis with physical health services under mental health parity regulations. This implies that insurance providers are unable to place more stringent restrictions on benefits related to mental health.

| Key Provision | Description | Benefit |

|---|---|---|

| Equal Coverage | Insurance plans must cover mental health services at the same level as physical health services. | Ensures fair access to necessary care. |

| Prohibition on Stricter Limits | Insurance companies cannot impose stricter limits on mental health benefits compared to medical/surgical benefits. | Protects patients from discriminatory practices. |

Mental Health Reimbursement Policy Fundamentals

Navigating the intricate healthcare system requires an understanding of the foundations of mental health reimbursement rules. These regulations specify the coverage of mental health services, including the costs and the reimbursement procedure.

In-Network vs. Out-of-Network Provider Coverage

In-network and out-of-network providers are frequently distinguished by mental health reimbursement policies.Patients usually pay less out of pocket when they use in-network providers since they have an agreement with the insurance company to deliver treatments at a negotiated rate. On the other hand, patients may have to pay ahead and then seek reimbursement from out-of-network physicians, who may not have such a contract.

Mental Health Reimbursement Rates and Structures

varying insurance plans have quite varying payment rates and mechanisms for mental health care. While some plans might have a set charge schedule, others might refund a portion of the entire cost. Predicting out-of-pocket costs requires an understanding of these rates.

Managed Care Requirements and Preauthorization

Managed care criteria, such preauthorization for specific treatments or a cap on the number of sessions annually, are a common feature of mental health payment policies.Prior to receiving treatment, preauthorization entails getting the insurance company’s approval to make sure the suggested care is both medically required and covered by the policy.

| Provider Type | Reimbursement Rate | Preauthorization Required |

|---|---|---|

| In-Network | 80% of negotiated rate | No |

| Out-of-Network | 50% of billed amount | Yes |

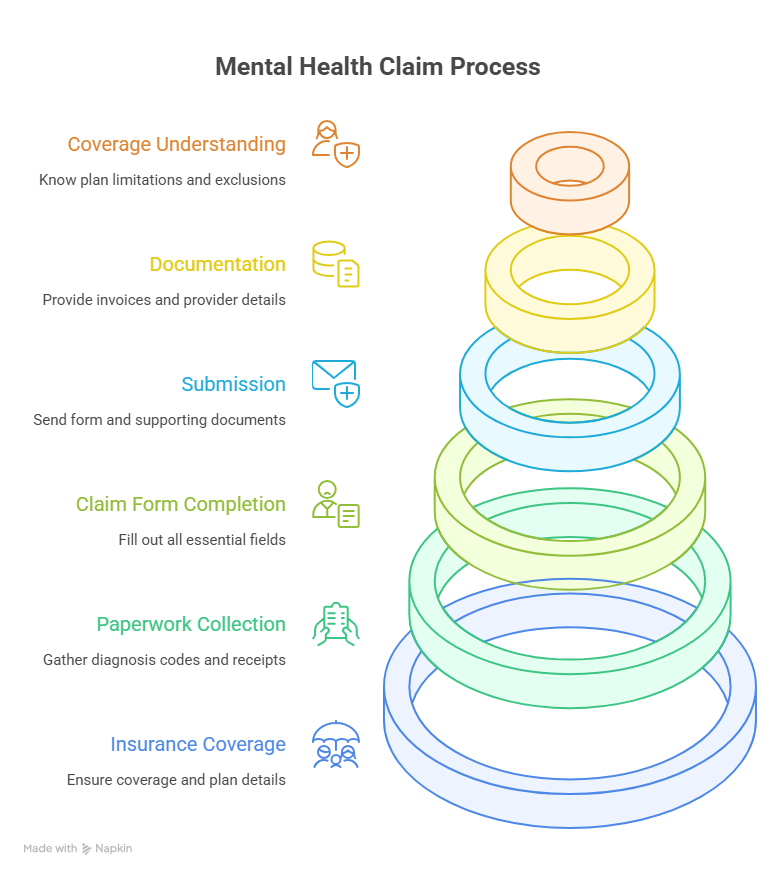

Navigating the Claims Process and Coverage Limits

Claiming benefits for mental health issues can be complicated, but it can be made simpler by breaking it down into steps. To make sure you get the coverage to which you are entitled, it is essential to comprehend how to proceed through this process.

Step-by-Step Guide to Filing Mental Health Claims

There are multiple steps involved in submitting a mental health claim:

- Make sure you are covered by your insurance and know what your plan covers.

- Collect the required paperwork, including diagnosis codes and receipts.

- Make sure you fill out all the essential fields on the claim form.

- Send your insurance company the claim form and any supporting paperwork.

Mental Health Billing Guidelines and Documentation

For claims processing to be effective, proper documentation is essential. This comprises:

- thorough invoices for the services provided.

- codes for diagnoses that match the services rendered.

- Provider details, such as name, address, and tax identification number.

Understanding Coverage Limitations and Exclusions

Knowing what your insurance plan does and does not cover is crucial. Typical restrictions consist of:

- annual session limits.

- exclusions from specific therapies or treatments.

- Out-of-pocket expenses are impacted by network limitations..

You can optimize your mental health benefits and more easily navigate the claims process if you are aware of these factors.

Maximizing Mental Health Benefits

It is essential to comprehend your mental health reimbursement policy in order to obtain the care you require. Understanding the nuances of your insurance coverage will help you confidently navigate the system. The purpose of the mental health reimbursement policy is to guarantee that you get the care you require by offering financial assistance for mental health services.

Understanding your policy’s coverage limits, deductibles, and copays is crucial to maximizing your mental health benefits. You can effectively plan your care and steer clear of unforeseen costs by doing this. If you have the correct information, you can stop worrying about the cost of your care and instead concentrate on your mental health.

You can take charge of your mental health care and make well-informed treatment decisions by adhering to the recommendations provided in this article. You can get the care you require to keep your mental health in good condition if you are aware of your mental health reimbursement policy.

FAQ

What is mental health parity, and how does it affect my insurance coverage?

The equal treatment of physical and mental health conditions in insurance plans is known as mental health parity. Insurance plans must offer equal coverage for mental health services, including treatment limits, copays, and reimbursement rates, in accordance with the Mental Health Parity and Addiction Equity Act (MHPAEA).

How do I know if my insurance plan covers mental health services?

To find out the extent of mental health coverage, look over the documentation for your insurance plan or get in touch with your insurer. Find out about any restrictions or exclusions, copays, deductibles, and mental health benefits.

What is the difference between in-network and out-of-network mental health providers?

A contract between your insurance company and in-network providers allows them to offer services at a discounted price. This contract does not apply to out-of-network providers, and you might be held more accountable for the expenses. Verify the reimbursement rates and whether your insurance plan covers out-of-network providers.

How do I file a claim for mental health services?

Your mental health professional will usually file the claim on your behalf. You might have to file the claim on your own, though, if you’re seeing an out-of-network provider. Find out how your insurer handles claims and what paperwork is needed, like a claim form and receipts.

What are some common limitations or exclusions in mental health insurance coverage?

Limits on the number of sessions, exclusions for certain diagnoses or treatments, and preauthorization requirements are examples of common limitations or exclusions. Examine the documentation for your insurance plan to learn about these restrictions and make appropriate plans.

Can I appeal a denied claim or coverage decision?

A denied claim or coverage decision may be appealed, yes. Verify the appeals procedure for your insurance plan, which usually entails sending in a written request along with any necessary supporting documentation. For help, you can also get in touch with the insurance department in your state.

How do mental health billing guidelines and documentation affect my coverage?

For insurance reimbursement, accurate billing and documentation are essential. To prevent denied claims or processing delays, make sure your mental health provider uses the appropriate codes and complies with billing regulations.

What are managed care requirements, and how do they impact my mental health coverage?

Preauthorization and utilization reviews are examples of managed care requirements that assist insurance companies in controlling costs and guaranteeing necessary care. To prevent unforeseen expenses or coverage denials, be aware of the managed care requirements specified in your insurance plan.